Enjoy unlimited access for less than $1/day

You'll receive unlimited access to all of our original reporting, plus newsletters, invitations to live events and more. Cancel anytime.

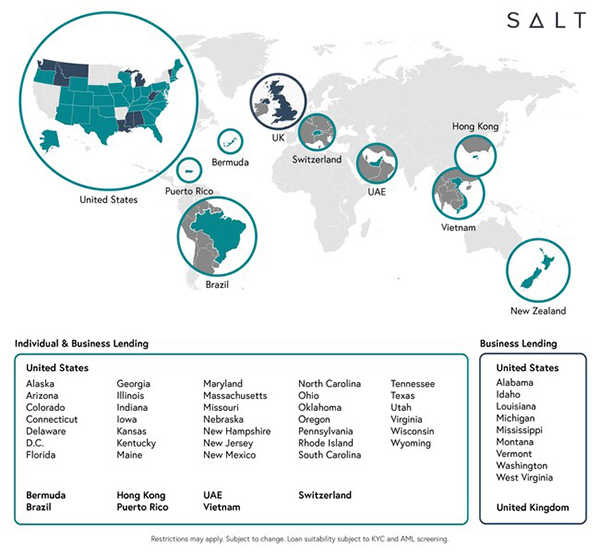

SALT recently underwent a massive domestic expansion and is now in 10 different countries. <em>(PRNewsfoto/Salt Lending Holdings Inc.)</em>

The Daily NewsFeed provides a quick summary of key local, state, and national business stories to start your day.

Sign up for free! or Become a Member Today